Loan Amortization Calculator – Make A Detailed Repayment Plan For Any Loan And Interest

Almost every business or individual needs to borrow money from time to time. And this is a completely normal procedure. If you are about to take a small business loan, you should very well plan how you will pay it back. One nice tool, that can help you do this is our online loan amortization calculator here. Using it, you will be able to get a complete idea about how your loan will be going. It will provide you with a simple and understandable repayment plan, which you can use to see how much you would pay for your debt. Just enter some basic parameters about it, press the button and you will see detailed information about the loan like monthly payments, monthly interest rate, total interest expenses, and some more information. The most valuable part of it, I think is the detailed repayment plan for your loan, where you will be able to see what exactly you would pay every month for interest expenses, principal payments, etc. If you have some difficulties using the calculator, see the instructions below.

This Is The Loan Amortization Calculator + Your Repayment Plan For The Specified Amount And Interest

Using The Loan Repayment Calculator

Here are some simple steps for using the loan repayment calculator.

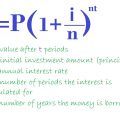

1. Enter the amount of the loan, without currency signs.

2. Enter the number of periods (usually months) until the loan is paid off. If the loan is for 5 years, the number of periods would be 5 x 12 = 60.

3. Enter the annual interest rate for the loan. You can type just numbers there ( 8.3 ), or use the percentage symbol ( 8.3% ).

4. Press the “Calculate” button and you will see the details for your loan in the right upper box and a nice payment plan in the big box.

Notice: These calculations may not be exactly what you would be offered. Banks and credit institutions may have some additional taxes, different conditions, etc. But here you can get a general idea about what your loan would be.

If you have a mortgage and you would like to see how much you have left from it, or just need to check whether or not your mortgage deserves refinancing, you can use our really cool mortgage calculator. It will show you not only a repayment plan for your loan but also will give you a nice chart showing its detailed amortization.

7 tips about what to be looking for when taking a loan

1. Interest Rates: Make sure you understand the interest rate associated with the loan and the potential for that interest rate to increase over time.

2. Loan Terms: Carefully review the loan terms for repayment, prepayment penalties, and other fees.

3. Credit Score: Before you apply for a loan, check your credit score to determine if you’re eligible and what interest rate you can qualify for.

4. Affordability: Make sure you can afford the loan payments, taking into account current expenses, debt repayment, and any additional unforeseen expenses.

5. Loan Duration: Consider the term of the loan and future expenses you may have to pay over the time period.

6. Other Details: Understand other details such as the length of time for loan processing, documentation required for a loan application, and any prepayment penalties.

7. Lender: Do your research and find a reputable lender that offers the best terms for your financial goals.

For small business owners, securing a loan can be a daunting process. Banks are often the go-to option for financing and getting the resources you need to grow, but credit qualifications and lengthy application processes can be a major challenge. Fortunately, there are alternative sources of financing and funding that can help you get the capital you need without the hassle.

Small business loans are specially designed to meet the needs of small businesses. These funds are generally easier to qualify for than traditional bank loans, allowing entrepreneurs with limited credit histories or collateral to get access to working capital for their businesses. Small business loans also tend to have shorter approval times and more flexible repayment terms than conventional financing options.

In addition to banks and other traditional lenders, there are organizations that specialize in business loans. These organizations typically focus on providing resources for specific industries or groups such as women-owned businesses or companies in rural areas. Many of these organizations offer free or reduced costs for applying for a loan, along with access to resources such as workshops and mentorship programs.

It’s also important to consider any government programs available when looking for small business loans. There are various initiatives from local, state, and federal governments that aim to support entrepreneurs who may not have access to more traditional lending options. The Small Business Administration is an especially good resource in this area, offering loans with favorable terms that are often easier to qualify for than those offered by banks or private lenders lenders.

When exploring loan options and applying for funding, it is important not to take on more debt than you can reasonably manage—or more debt than your projected income allows you to pay back comfortably within your desired repayment period. This way you can ensure that taking out a loan will actually help your business remain profitable over time instead of creating additional financial burdens down the road.

How do you like this post? Tell us, so we are able to improve your experience.

Check some other cool startup articles:

Mortgage Amortization Calculator With PMI, Taxes and Insurance

Mortgage Amortization Calculator With PMI, Taxes and Insurance

What Is Compound Interest And How To Calculate It? The Compound Interest Formula

What Is Compound Interest And How To Calculate It? The Compound Interest Formula

Compound Interest Calculator – Calculate The Growth Of An Investment Over Time

Compound Interest Calculator – Calculate The Growth Of An Investment Over Time

A Simple Business Plan Template To Help You Create Your Own Plan

A Simple Business Plan Template To Help You Create Your Own Plan

What Is Gearing? A Simple Definition

Monthly Compounding Interest Calculator Online

What Is Financial Leverage? How leverage Works – For Dummies

What Is Gearing? A Simple Definition

Monthly Compounding Interest Calculator Online

What Is Financial Leverage? How leverage Works – For Dummies